The task of purchasing a property can be extremely difficult, whether you've done it before or not. The temptation is to either settle for the first house that fits your budget or to keep renting.

In this post, we’ll explore what you should think about before you buy, what to expect from the actual buying process, and some practical advice to make life easier once you move into your home to help you demystify the process and make the most of this purchase.

This will help you navigate the difficult process of getting started, setting a budget for a home, looking for one, inspecting it, understanding the fundamentals of buying, and obtaining a mortgage.

Your long-term goals are the first thing you need to decide. After then, think about how owning a home fits into those plans. Some people simply want to convert all those "wasted" rent payments into mortgage payments that result in equity. Others appreciate the thought of being their own landlord and view homeownership as a symbol of their independence. Then there is the problem of considering home ownership as an investment.

You can move in the right direction by focusing on a smaller range of your long-term homeownership objectives.

A classic single-family home, a townhouse, a condominium, a co-operative, or a multi-family complex with two to four units are all possibilities when buying a residential property. Depending on your ambitions for homeownership, every choice has advantages and disadvantages.

You must decide which kind of property will enable you to accomplish those objectives. By selecting a fixer-upper, you can also reduce the cost of your purchase in any category (although the amount of time, sweat equity, and money involved to turn a fixer-upper into your dream home might be much more than you bargained for).

You're making what may be the largest purchase of your life; while it's wise to keep some flexibility in your list, you still deserve to have it as near to your needs and wants as possible.

Your wish list should cover everything from the most fundamental considerations, such as neighborhood and size, to more specifics, such as bathroom design and the presence of reliable appliances in the kitchen. To find a new house that meets your needs and preferences, real estate websites can be an invaluable resource.

Knowing how much a lender will actually loan you to buy your first house is vital to know before you start looking. You might believe you can afford a $300,000 home, but lenders might only think you qualify for a $200,000 mortgage, depending on things like your overall debt load, your monthly salary, and how long you've had your current employment.

Before making an offer on a home, make sure to get pre-approved for financing. A lack of a mortgage pre-approval will frequently prevent sellers from even considering an offer. Furthermore, a lot of real estate agents won't waste their time talking to clients who haven't made it clear how much they can spend. Compare loan rates and costs for lenders as you start your search. After that, submit your mortgage application along with any supplemental materials your lender may need to confirm your debt and income.

But occasionally a bank will provide you with a loan for a home that is more expensive than you actually wish to pay for. You shouldn't borrow $300,000 just because a bank says it will unless you really need to. Many first-time homebuyers make this error and end up "house-poor," which means that after paying their monthly mortgage payment, they have little money left over to cover other expenses like clothing, electricity, vacations, entertainment, or even food.

You should consider the entire cost of the house when choosing the size of the loan, not simply the monthly payment. The amount of homeowners insurance you'll need to buy, the amount you'll have to spend on upkeep or improvements to the house, the number of closing expenses, and the amount of property taxes in your preferred neighborhood are all things to take into account.

Your down payment (3.5%–20% of the purchase price) and closing expenses will need a large upfront cash outlay, even if you qualify for a sizable mortgage.

One of the major obstacles when it comes to investing with a short-term objective in mind—buying a house—is maintaining assets in a reachable, reasonably secure vehicle that yet offers a return. A certificate of deposit (CD) might be an excellent choice if you have between one and three years to reach your goal. You won't get wealthy, but you won't lose any money either.

Buying short-term bonds or a fixed-income portfolio may be thought of in the same way; they will provide some growth while also shielding you from the volatile stock market.

You will want to keep the money liquid if you plan to buy a house within the next six to twelve months. The ideal solution might be a high-yield savings account. If the bank fails, you will still be able to access your funds up to $250,000 if it is FDIC insured.

Your needs and your budget will be taken into account while a real estate agent helps you find properties. They'll then meet with you to show you those houses. These experts can help you with all aspects of the home-buying process after you've decided on a house to buy, including making an offer, obtaining financing, and filing the necessary paperwork.

Any mistakes you may run into during the process can be avoided thanks to the experience of a professional real estate agent. The majority of agents get compensated out of the sale proceeds as a commission.

These are just some of the questions you can ask yourself when buying a home. In Part 2, we’ll dive deeper into the process of buying a home.

Investing in a home is both an emotional and sustainable investment. It is the place that will provide you with shelter and security and it is also the precious space you will spend your days and nights in you will call home and make memories in. In this article we are bringing you 5 reasons why you should invest in a home. We will also link you to 3 of our amazing agents that you can get in contact with to simply ask questions, or if you’re interested, start browsing homes that meet your financial and location needs. Let’s dive in!

One of the greatest qualities of owning a home is the ability to transform your home into whatever you need it to be as you and your family grow over the years and needs change. An example would be the unexpected pandemic of COVID-19. This pandemic has made a big impact in remote working. During lockdown, we were able to work from the comforts of our own home. Of course everyone made due with the space they had, but those with a home office were able to sit down comfortably and have a proper working environment and space. Qualities that make a great home office include space, being closed off from active and noisy areas of the home and windows to invite lots of natural light in.

In an apartment, it’s easy to feel overly cautious of the noise you make in having neighbors on your left and right, and below you and above. With your own home, you can relish in increased privacy, something apartments can’t offer. This increased privacy comes with increased space as well which is another win to collect in having a home versus an apartment.

Some tax benefits you as a current or future homeowner can expect to benefit from include deductible interest in many cases, the amount you pay in property taxes is deductible, collect tax deduction points over the period of your loan, PMI (private mortgage insurance) can be deducted in some cases and if you work at home you can deduct your home office expenses and the space that is used.

In renting an apartment, tenants can expect to have some amount of increase to their rent every year as the cost of living increases. In owning your own home you can find financial comfort in having predictable monthly payments, avoiding the annual increase in home finances that apartment renters find themselves in.

The last reason on our list as to why you should invest in a home is that you get to take pride in ownership. Feel great about owning the precious space that you call home, being able to modify it freely as your needs grow and enjoying increased space and privacy.

It used to be that you could easily purchase a home with just a 10% down payment. During the housing boom (before the burst) you could sometimes get a home with as little as 5% or even 0% down. These days, though, it's much more common to see people putting 20% down on Indianapolis homes. The trend is largely due to the recent housing crisis and lenders having a bit less faith in the people who are borrowing. As a result, it's harder for many Hoosiers and people across the nation to purchase the homes that they want and feel that they can afford. Leading up to the housing crisis, banks were being somewhat irresponsible and giving loans to people who couldn't actually afford them. Because of these past mistakes, lenders are now being much more stringent about who they offer loans to. Having 20% down on the home you would like to buy is a solid indicator that you are ready to make the purchase, and banks like to see that. For some people, however, getting together 20% takes a great deal of time. If you're looking to get into a new home within the next few months but have less than 20% to put down, talk to an experienced Indianapolis real estate agent, like the team members at RE/MAX Advanced Realty, to learn about your options.

Options your realtor may discuss with you include alternatives to traditional home loans like VA loans and government mortgage assistance programs. For example, if you’re a first time homebuyer, you may qualify for a FHA loan through the U.S. Department of Housing and Urban Development (HUD). With a FHA loan, you can put down as little as 3%, sometimes less. However, keep in mind that the higher your down payment, the less expensive your monthly mortgage will be. Another way to avoid a hefty down payment is to consider other housing options. By turning to a professional realtor, you can become informed of housing that will still work for you and your family, but at a lower price point. For example, instead of considering a three-bedroom single-family home, you may consider a condo or townhouse instead. In many cases a townhouse can give you almost as much room as a single-family home and at a significantly lower price. Whatever your situation, it's a good idea to make sure you have a solid plan in place for affording your home before you make any buying decisions. Working with an experienced realtor can help you determine precisely how much house you can actually afford. Once you have your parameters in place, your realtor can help you find something that will work within your budget. You may be surprised what you are able to find in Indianapolis without having to count pennies. Working with the best realtors in the area will give you access to listings you might not have been able to find on your own. Call RE/MAX Advanced Realty today at 317.298.0961 to learn more.

If purchasing a home is on your bucket list, there are six considerations to make that may improve your ability to obtain a mortgage.

In order to ensure that you can make your recurring home loan repayments, lenders will carefully examine your credit report. Therefore, if you're thinking about buying a house, it's crucial to make sure that you're paying all of your expenses on time and avoiding being late with any repayments.

Contrary to popular belief, reviewing your credit report won't actually harm your score as a whole.

Actually, there are two different ways that your credit score can be checked. A "soft" inquiry, such as checking your personal credit record, won't lower your score. Giving a lender your consent to examine your credit report, however, is regarded as a "hard" inquiry and does have an impact on your credit score.

Here are some tips to improve or maintain a good credit score:

Record all your financial transactions made using your credit and/or debit card, including any checks you’ve written using your ATM card. You can check your transactions online to keep track of your balances, confirm deposits, and see other activities. You should report any potential anomalies right once.

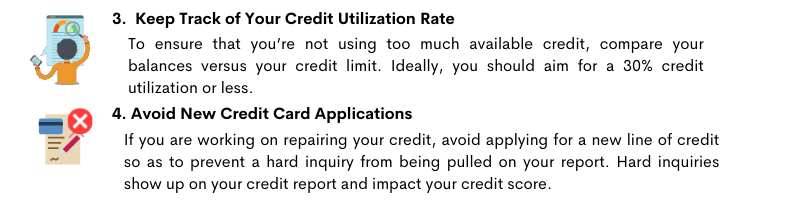

Your available credit, which is the amount of credit left on a line of credit or credit card after deducting any existing debt, is the credit limit. Verify that you are not using all of your credit limits or exceeding them, as this can hurt your credit score.

Pro Tip: Keeping your credit utilization rate below 30% may help you maximize your credit score.

Maintain a reserve of credit equivalent to at least 15% of your available credit for emergencies. Or even better, maintain a liquid, interest-bearing account with three to six months' worth of living expenses set aside as an emergency fund. In this manner, you avoid taking out more debt than you are comfortable repaying in case you lose your job or incur a big unforeseen expense.

Pro Tip: Setting up recurring payments into a savings account through your bank can help you with building an emergency fund.

Consistently make your minimum required monthly payment on time each month. You can lower your loan charges by paying more than the minimum each month—or, even better, the entire sum. Make sure you don't miss any payments.

Making on-time payments is a key step in raising your credit score because your payment history accounts for about 35% of your FICO® Credit score. When your payments are due, think about setting up alerts.

When you apply for a mortgage, the lender will ask you for certain information so they can fully assess your financial status. For this reason, it's a good idea to keep your most recent loan and credit card statements, savings account data, pay stubs, and tax returns close to hand to speed up the house loan application process.

Think about locating the ideal family-friendly dream home.

Finding the ideal lender to help realize this dream of house ownership is all that is required when the home inspection process is completed successfully. It might be challenging to choose the best mortgage lender from the many options accessible today, including local banks and internet mortgage lenders.

The house-buying process requires selecting the best mortgage provider, which can be a difficult task. Just keep in mind that there are several crucial qualities to look for when choosing the proper lender:

Although starting your own business after leaving the corporate sector can be an exciting career transition, it may have an impact on your ability to borrow money when applying for a home loan.

Starting a new business may result in uneven cash flow at the outset of the endeavor or a lack of standard documentation. Some lenders may evaluate your income and savings, among other things, throughout the application process.

Lenders want to see evidence of your ability to save money. Most people search for what they consider real savings. So it makes sense to transfer any extra money into a separate savings account and to continue making regular deposits.

These are just some of the things you need to consider when you apply for a mortgage loan. For more tips like this, check our website or follow our official social media accounts.

If you’re new to real estate, whether as a buyer or an agent, decoding the industry itself can be challenging.

It’s complex to learn the process of selling, buying, or investing alone, and so is learning all its jargon. However, it’s critical to know even just the basics before you dive into it to avoid further confusion.

In this post, we’ve listed some of the commonly used real estate terms to know.

In layman’s terms, it is a mortgage with a variable interest rate. During the initial period, the interest charged to the loan is fixed, but after that, the rate will adjust at monthly or yearly intervals.

To determine the approximate worth of the real estate, an appraisal is necessary. The mortgage lender sends a property appraiser to assess the asset's worth. This helps the lender determine if the amount that the borrower is asking is worth it.

If the appraised value of a home is less than the sale price, an appraisal contingency allows a buyer to cancel the purchase agreement.

To guarantee that the loan is secured by a suitable house value, the buyer's lender hires an appraiser to assess the worth of the property. Lenders want to make sure they aren't "overpaying" for a piece of real estate.

If the initial transaction fails, a buyer who is interested in buying a property that is already under contract with someone else has the option to make a "backup offer." To ensure that a backup offer is the next in line, it must still be negotiated and any funds, like earnest money, must be provided. Legally, there can only be one backup offer because a backup to the backup cannot exist.

Even when viewing the property as possible, a buyer making an offer on it without seeing it was deemed as a "blind offer." It is an approach frequently used in highly competitive situations.

A buyer's agent also referred to as a selling agent, is a qualified real estate agent whose responsibility is to find a buyer's next home and to represent that buyer's interests by negotiating on their behalf to secure the best possible deal.

A neighborhood association, a homeowner's association (HOA), a builder, or a developer will typically impose these rules and regulations on real estate to outline any requirements and restrictions on what a homeowner is permitted to do with the property. Additionally, it could include special, yearly, or monthly assessments.

The owner could sell their home when the said property is owned outright (has no outstanding debt on the mortgage) or the owner owes less on their mortgage than what the market suggests they may get for it.

When the home transaction closes, it is deemed complete. Typically, this occurs when all parties have signed the necessary paperwork, transferred all funds, and if a lender is involved, received full lender approval. The very last stage of closure for several marketplaces around the country is documenting the deed with the county clerk's office. Considered the new homeowner, once each of these requirements has been met, the buyer is granted entrance to the residence.

DOM for short is the period between the day a property is advertised for sale on the multiple listing service (MLS) of the neighborhood real estate brokers and the day the seller and buyer enter into a contract to sell the property.

A mortgage lender's debt-to-income ratio, or DTI, is calculated by dividing your monthly housing payment and all other debt payments by your gross monthly income and multiplying the result by 100. This enables lenders to estimate how much you can afford to pay monthly for a mortgage by using their available lending programs to calculate affordability.

When a seller accepts a buyer's offer, the buyer will be required to make an earnest money deposit (EMD), sometimes known as a "good faith deposit". It demonstrates the buyer's seriousness about the purchase as well as their willingness to back up their words with deeds.

The EMD might be between 1 and 5 percent of the sales price in amount. The EMD is frequently kept by an escrow business or by other provisions of the purchase and selling agreement (PSA).

This is the depositary (impartial third-party) and agent who gathers the funds, necessary documents, personal property, written instruments, and/or other items of value to be held until specific events or the performance of described conditions happen, usually outlined in mutual, written instructions from the parties.

Equity is the investment made by the homeowner in their house. Your home's equity is calculated as the amount that is left over. To get this, take the home's market worth and deduct any mortgages or liens from it.

A set of loans that are insured by the federal government includes FHA loans. In other words, the FHA insures banks and other private lenders against potential losses they might sustain if the borrower does not repay the loan in full or on time.

Known as a "fixer-upper," this combines a mortgage loan with a loan to help pay for improvements or repairs, like structural or energy-related changes. However, it can't be used for luxury improvements, such as adding tennis courts or swimming pools.

As the name suggests, the interest rate will not change during the term of a fixed-rate mortgage. They are frequently offered as 10, 15, 20, and 30-year loans.

Hard Money Loan

An alternative to using standard lenders is to take out hard money loans. Hard money lenders often demand a sizable down payment and a quick payback plan and base the loan's eligibility on the property in issue rather than the credit score.

A private organization called a homeowner's association oversees a condominium or planned community. You agree to adhere to the HOA's rules and pay monthly or yearly HOA dues when you purchase a property that is managed by an HOA. They frequently have the right to foreclose on the property if you don't pay and/or don't comply, and/or they can file a lien against the property.

Using a house sale contingency, a buyer might tell a seller that one of the requirements for buying their property is that they can successfully close on their existing home. This is frequently negotiated as part of a clause or addition to a contract. If a buyer needs to sell their home to have the down payment needed to buy the new home or would prefer to utilize the sale money rather than their savings to make the down payment, then such a contingency could be employed.

Inspection is a process wherein a potential home buyer hires a certified professional inspector to visit the house and create a report on its condition and any required repairs. The inspection frequently takes place during the period of due diligence so that buyers can decide for themselves whether they want to purchase a particular home as-is or ask the seller to make or pay for specific repairs.

The inspection contingency, sometimes known as a "due diligence contingency," is a provision occasionally included in a purchase agreement that gives buyers a certain period during escrow to do any required inspections.

Traditionally, when you buy a house, you become the owner of both the building and the land it is situated on. A land lease may be necessary in some situations, in which case you would own the house while paying the landowner's rent.

A loan contingency is a clause or addendum (also known as a mortgage contingency) in an offer contract that permits a buyer to back out of a purchase and keep their deposit if they are unable to get a mortgage with specific parameters within a set amount of time.

Property purchasers must obtain a mortgage pre-approval letter because it outlines their financial capabilities. After examining the buyer's debt-to-income ratios, cash on hand, and credit history, the lender issues a mortgage pre-approval letter outlining the terms, loan type, and loan amount the buyer qualifies for.

Real estate agents and broker members use a database that gives them access to modify or add information about properties that are available for sale in a specific area, and this is called Multiple Listing Service (MLS). The MLS is frequently checked by buyer's agents to see what properties are available and what they have recently sold for.

Most states require this report, and this discloses when a property is situated in an area where there is a higher risk of natural disasters. Typically, the seller pays for the study and provides it to the buyer during escrow.

In an NHD report, the following natural hazard zones are included:

Customers submit a formal offer for the house they wish to buy. Depending on what you and your agent believe to be the fair market value, the offer may be the full list price.

After getting your signature and putting the offer in writing, the buyer's representative sends it to the seller's agency for consideration. The seller has two options: either accept it right away, in which case it becomes the parties' purchase contract, or make a counteroffer. It is the art of negotiation that is documented in writing.

Homebuyers must complete an application to obtain pre-approval, which enables a lender to assess their financial condition, including their debt-to-income ratio, repayment capacity, and creditworthiness. Once this is obtained, the lender can provide a letter to the buyer indicating the precise loan amount for which they have been pre-approved as well as the total sales price for which they are approved.

Typically, the letter will state the projected interest rate as well as the buyer's anticipated down payment. The majority of sellers want to see a pre-approval letter along with an offer because it is far more detailed than a pre-qualification letter.

To deliver a clear title, the seller must take care of any title problems that are revealed by a preliminary assessment. The information provided includes easements, liens, and the history of ownership. By looking through the county recorder's office's database of past property transactions, the title business compiles this report.

Before a title insurance provider may provide title insurance coverage, they must receive this report. To safeguard their interest in a property, most lenders require borrowers to buy title insurance coverage. Even though it is a negotiating point, it is common practice in many places for a seller to cover the cost of this insurance.

The sum of money owed to the lender on a mortgage loan, excluding interest, is known as the principal balance. Take a loan of $300,000. That is the loan principal or the amount you borrowed to purchase the house. The interest, which is computed daily for the majority of loan types, is paid by buyers each month together with the principal. Almost always, interest is paid on payments before the principal is deducted. After all, the bank only agrees to provide the loan because of the interest.

When a homeowner passes away without creating a will or deciding to give a property to someone, a probate sale takes place. The probate court would then provide permission to an estate lawyer or other representative to engage a real estate agent to sell the house under such circumstances.

The entire process will typically be a little more difficult and time-consuming than a typical transaction.

The term "real estate owned" refers to homes that a lender now owns after an unsuccessful auction foreclosing on them.

REO homes occasionally offer a chance for a buyer to purchase a property for less than market value because the majority of banks would rather reinvest the proceeds than waste time promoting the property for a prolonged period.

Financing can be challenging because the bank frequently markets the property "as-is," meaning they are not willing to make any modifications to it.

Although the terms "REALTOR®" and "actively licensed real estate agent" are frequently used interchangeably, not all real estate agents are REALTORS®. A member of the National Association of REALTORS® is a REALTOR® (NAR).

A REALTOR® commits to maintaining the association's Code of Ethics and to keeping one another responsible for providing the public, customers, clients, and each other with high-quality service.

When a buyer, who is now the new homeowner, agrees to let the seller, who is now the tenant, remain in the home after escrow closes, this arrangement is referred to as a rent-back, sometimes known as a leaseback. In advance of the event, the terms are agreed upon, and they frequently include a leasing deposit, a daily rental charge, and a permissible time frame.

It is occasionally feasible to calculate the rate by taking into account the new homeowner's monthly mortgage out-of-pocket costs as well as any potential trouble this may cause them by postponing their move.

To get purchasers to buy the home or make the deal more appealing, sellers may make concessions.

Up to certain restrictions and with the lender's consent, concessions are most frequently considered as a contribution toward the buyer's closing costs, which, in the end, puts more money in the buyer's pocket.

A seller's disclosure is a statement made by the seller that, to the best of the seller's knowledge, contains facts about the property or that could influence a buyer's choice to buy the property.

In addition, a seller is required by law to disclose any information that may affect a buyer's enjoyment of the property but is not directly related to it, such as pest issues, boundary disputes, knowledge of significant construction projects nearby, military base-related noises or activities, association-related assessments or legal issues, unusual odors from a nearby factory, and even recent fatalities on the property.

When a property is sold short, the amount received for it does not cover the loan it is used to secure. Since the proceeds of a short sale will fall just "short" of the debt, the lender(s) of the seller will need to approve the transaction. Because most lenders' clearance procedures for short sales are drawn out and time-consuming, a short sale will take longer to finalize than a standard one.

The seller is not allowing the property to be examined before an accepted offer when they use the phrase "submit offers subject to inspection" or "submit offers subject to inspection". Tenants who are uncooperative or who have privacy concerns are two prominent causes of this.

You can take advantage of the typical buyer's apprehension regarding buying a house without seeing it because it will surely reduce interest in the market as a whole.

Additionally, it's not as bad as it first appears because, under the typical purchase agreement, there will be an inspection period during which you can end the deal without incurring any fees.

A sort of joint ownership of a property, whether it be a single-family home or a business building, is referred to as tenancy in common. The property is owned by all of the common renters, though in various proportions.

The simplicity or complexity of obtaining finance will depend on the type of property. Additionally, tenants in common do not have the right of survivorship, therefore the deceased tenant's ownership stake or percentage truly belongs to their estate, as determined by their will or the applicable law, rather than the remaining owners receiving a share of it.

Small, whitish, soft-bodied termites feed on wood and can cause a lot of damage. A diagram of the property and the locations of current and/or past WDI activity are included in the WDI report, often known as the termite report.

The report may also, and in some cases, mention what could be required to deal with such potential infestations, such as spraying or tenting. The cost of such products won't typically—if ever—be mentioned in the WDI report because it might be seen as a conflict of interest.

During a title search, the history of the property is analyzed from public documents, including sales, purchases, tax liens, and other types of liens.

To find out who is listed as the property's official owner, a title examiner will often search title plants and occasionally county records. The Preliminary Report will detail this information, along with any liens or encumbrances that are recorded against the property, for the parties to evaluate before the conclusion of escrow.

In a trustee sale, the seller is a trustee of a living trust rather than a private individual. Most frequently, this is due to the original homeowner's passing away or the placement of their assets in a living trust.

Since the trustee may choose to sell the property, they might accept a less desirable offer because they are not as emotionally invested in it as a regular owner would be.

A VA loan is a mortgage loan provided by the U.S. Department of Veterans Affairs.

Veterans, active duty personnel, and the surviving spouses of these individuals can obtain VA loans to buy homes with a small downpayment, no private mortgage insurance, and better interest rates.

These are just some of the real estate terms to know.

For more content like this, be sure to visit our website or follow our official Instagram account.

Getting a Mortgage Loan is a complex process, and upon application, the lender shall conduct a deep dive into your financial life to ensure that you meet all of the underwriting requirements. Get organized and ready to save time and avoid stress by preparing this list of essential documents needed to make the process smoother and to improve your odds of getting approved:

Mortgage lenders want to know your financial situation and ensure that your annual income is consistent with your reported earnings through pay stubs and that there aren't huge fluctuations from year to year.

Generally, they want to see 1-2 years' worth of tax returns, and you will most likely be required to sign Form 4506-T, which allows the lender to request a copy of your tax returns from the IRS.

A verification to prove that your income is as you have stated is required by your lenders through documents, including recent paycheck stubs and your most recent W-2 form.

Your lenders will assess your risk profile by looking at your bank statements and other assets- including checking, saving accounts, investments, and insurance.

Typically, they look at two months of recent bank statements to verify your savings and cash flow; check for unusual deposits, withdrawals, or any other activity in your accounts.

Self-employed borrowers who want to qualify based on bank statements instead of tax returns need to provide the past 12-2 months of bank statements.

A credit report shall be pulled through verbal or written permission to assess a borrower. Lenders look at credit history to assess your relationship with loans and money in the past. It's a way of them knowing whether you're likely to pay your loan as agreed or if there's a high risk for default.

A valid ID is required to prove that you are who you are claiming to be.

Here's a list of the acceptable IDs

( for those who don't own a home yet)

( for those who own another property)

Renting history is important, especially if you don't have an extensive credit history. Lenders will request proof that you can pay on time. If you don't own a home yet, they may ask for a year's worth of checks that your landlord has cashed, plus a documentation from your landlord showing that you paid rent on time.

Those who own another property need to provide the address, property value, status of the property, intended occupancy, whether rental, investment, or a second home, and monthly expenses related to the property. Properties with an outstanding mortgage also need to provide lender and loan details.

Please note that requirements may still vary from lender to lender. Get in touch with any of these most trusted lenders by our realtors for a list of paperwork you might need to provide based on your circumstance.

Angel Shelton | Bailey & Wood

Angie Turley | Team Turley | Fairway Independent Mortgage Corporation

Austin Smith | Fairway Mortgage Corporation

Bill Mynatt | Fairway Independent Mortgage

Celeste Meyer | GVC Mortgage

Christian Campos | The Federal Savings Bank

Jeffrey Arthur | Fairway Mortgage Corporation

Jody Bleier & Brian Brent | Bailey & Wood Financial Group

Joe Rangel | CrownMark Mortgage

Kathy Dillon | Fairway Mortgage Corporation

Kevin Walters | Walters Mortgage Team | Bailey & Wood Mortgage Lender

Mike Bentley | CrossCountry Mortgage

Mike Wood | Bailey & Wood Financial Group

Paul J East | Advisors Mortgage Group

Stacey Mayo | Ruoff Mortgage

Tony Lamonaca | Cross Country Home Loans

Zak Shobe | MJW Mortgage

Don't forget to contact our RE/MAX Advanced Realty Agents to help you throughout your home-buying process.

One of the most important measures of your financial health is a good credit score. A good credit score shows the lender how responsibly you use your credit. The better your score, the easier it is for you to qualify and be approved for better interest rates on new loans or lines of credit. A poor credit score, on the other hand, makes it harder to get qualified for a new loan or open a credit line. It also puts the borrower on the hook for higher interest rates. Thus, a good credit standing is very important in today’s society that has become increasingly dependent on credit to make purchases and financial decisions.

If you currently have a poor credit score, here are some of the steps you can take right now to improve it:

The tips mentioned above are just some of the ways you can improve your credit score. If improving your credit score is a goal you have, keep in mind that the sooner you begin working to improve your credit, the sooner you will see results.

2019 is quickly coming to a close, and it’s the time of the year to reflect and create goals for the new year. If purchasing your dream home is one of your goals this 2020, here are some New Year’s Resolutions you can implement into your lifestyle to keep your financial resume in tiptop shape and prepare you for your dream home.

Avoid Changing Careers

Employment history, alongside income, will be a major factor during your mortgage application evaluation. While a new job could be a good career move, most evaluators are looking for a steady job history with little to no gaps in your employment over the last few years.

Focus on Building Your Credit

--- Check Your Credit Score

Your Credit Score determines your creditworthiness; which banks and lenders use to determine if you qualify for a loan, at what interest rate, and what credit limit.

Be sure to monitor your credit closely. If you’re unsure of your credit score, there are numerous financial websites that offer credit score monitoring. Plus, most of these credit sites will tell you what impacts your credit most. Be wiser this coming new year and change your spending habits. If you have large debts negatively impacting your credit, get started on a payoff plan so your score can improve.

--- Build A Solid Credit History

The first thing that a lender will check is your credit history. Create a solid credit history by paying off debts and paying bills on time. Borrowers who have a history of paying off credit cards and other debts on time are preferred by lenders; as this signifies that you are less of a risk and a responsible borrower.

No credit yet? Don’t be disheartened. Securing a home loan can be more challenging and time-consuming, but not impossible. Your potential lender can look into your history of managing monthly payments and gauge if you are a responsible borrower through your on-time payment of rent and utilities, student loan debt or cell phone bills.

Cut Down Expenses. Create a Budget and Stick to it.

Is there a monthly expense you can possibly cut down? The monthly subscriptions that you don’t actually use for example? How about limiting dining out and only buying things that are necessary?

--- Cut Down on Monthly Subscriptions

Although convenient, monthly subscription services can add up and you could be dinged for high credit utilization if your credit report is pulled midcycle even if you pay off your credit card every month.

Limit your monthly subscription services to those you ACTUALLY NEED. Do you really need a cable subscription these days?

--- Spend Wisely

How many times do you eat out? According to Business Insider, people in Indiana spend an average of $2,241 on dining out (Business Insider (2019): Here's what the average person spends on dining out in every state). This amount can already be thrown towards your down payment fund. So instead of eating out, pack your lunch. Not only do you save money, but you can also prepare healthy meals.

--- Avoid Large Purchases

REMEMBER THE GOAL: BUY YOUR DREAM HOME! Don’t take on large amounts of debt- may it be a vacation or buying a car - before buying a house.

Your debt-to-income ratio plays a pivotal role in your loan approval. If you make large purchases, the ratio could sway in the wrong direction.

Just like anything worth having, preparing to buy your dream home won't be easy. You will have to make adjustments and sacrifices to achieve your goal. Luckily, there are many online tools and resources you can use to aid you in determining the factors necessary in buying a home, such as the Motto Mortgage Experts menu of home loan calculator that will give you an idea of how much home you can afford as well as provide custom down payment estimates based on home price and interest rates.

So, you’re ready to buy a home. You’re asking around and your family and friends have a lot of input, but you can’t help but to think...are they even remotely informed? And why are people who still rent apartments telling me how to buy a home? Shouldn’t I be talking to someone who does this for a living? Have no fear, your instincts are correct!

The Indy Home Pros Team has been ranked the #1 Real Estate Team in Indianapolis by The Indianapolis Business Journal for 4 years running, and we do not take this honor lightly. We specialize in ensuring your first time home buying process goes as smoothly and as magically as possible. Sure, there are hundreds of pieces of paper and documents that go into buying a home, and there should be; it’s the biggest purchase of your life! But we take care of that, that’s our job, not yours!

There can never be a complete guide to buying a home, because each home buying experience is unique to you. So below are some quality steps to take instead, and if followed, will get you through it!

1) Get Pre-Approved

All this means is that you call a mortgage broker (most likely your friend you see spamming your Facebook Feed that you have no idea what they do for a living, yes, that’s a mortgage broker) and give them some info about your life. i.e. how much money you make, how much debt you have, and they will come back to you, hopefully, with a money amount that you are able to safely spend on a home, say, $145,000.

2) Find and Hire a Realtor

Just because your Uncle Billy Bob is a realtor does not mean you have to use him. In fact, you likely shouldn’t. Didn’t he have one too many and fall off the porch last Christmas? Is that really who you want showing you houses? Plus how awkward will it be when you have to fire your own kin? Distance yourself slowly and pick an Indy Home Pro instead!

The market has changed since the 1990s and you need a realtor who is active and knows the current market and trends, knows all the relevant paperwork and how to execute it QUICKLY, has relationships in the industry with current title companies and so on and so forth, things you don’t need to think about because you are using a realtor!

That’s it! You’ve done your job, now let your Realtor do theirs! Just Kidding. Much more valuable info is below!

3) Don't eliminate homes that aren't up to par in your eyes as there are loans available to assist in renovating properties before you move in.

These are 203K loans that will allow for budgeting in renovations prior to close and can range from a simple bath or kitchen remodel to a full blown, top to bottom overhaul.

4) If financing is an issue, check with family to see if they can gift you funds for a down payment. This is allowed and can help new home buyers get things off the ground for your first time around.

5) Seek out lenders that can offer 0% down assistance to first time home buyers. Additionally, be aware that there are government loans that allow for the same type of financing as this in the form of a VA or USDA (rural) loan.

You’re setting out to buy a home and it’s likely one of the most exciting, and stressful, times of your life. And while it can be tempting to jump on a home search site that rhymes with pillow and go for it, you can now avoid the common pitfalls of first time homebuyers by naking sure you don’t commit any of these 5 mistakes that others have already made for you!

Like we said above, it can be tempting to get online and GO FOR IT! But then, you find it, the house of your dreams! BUT! By the time you find a realtor and try to set up a showing, someone else submitted an offer and it was accepted. But how? How were they so quick? They were Pre-Approved!

Getting Pre-Approved is the first, and arguably most important, step in the home buying process. Getting Pre-Approved is as simple as contacting a Mortgage Lender, filling out a form, and then seeing how much house you can afford based on things like your income, debt, savings, etc.!

Depending on where you are buying your home, your personal background, and various loan options; you could qualify for a first time home buyer program! This could mean a significantly lower down payment than the once standard 20%, lower monthly payments, and other saved costs!

Most new home buyers start their home search by looking at existing homes, and don’t ever consider building a new home because they think it’s too expensive. This is no longer the case these days! Companies like M/I homes offer SMART Options, meaning a brand new home in a community like Fisher’s can be yours for less than you think!

Checking your credit report to make sure it’s accurate. Lenders will go over your credit report with a fine tuned comb, so making sure everything on your report is correct is essential in getting the best loan rate and option for you. Pull your report from one of the major 3 companies, or use another credible site. Take it up with one of the 3 major companies if there is something on there you find incorrect.

Before your mortgage is final, do not mess with your credit! This means no applying for a new credit card, no booking that European vacation via credit, or anything else credit related. Applying for or adding new credit has the potential to lower your credit score, and this could in turn have an impact on your loan.

8313 W. 10th St

Indianapolis IN 46234

dennis@indyhomepros.com

317-316-8224